As Indonesia embarks on a new fiscal era under President Prabowo, the government is contemplating bold policy measures: increasing the debt-to-GDP ratio from 39% to 50%, raising the budget deficit from 2.35% to 5%, and boosting the tax-to-GDP ratio from 10.6% to 16%. These steps aim to finance infrastructure projects, social programs and an 8% growth rate but they also carry significant risks that must be carefully managed.

Indonesia's Debt and Deficit in Global Context

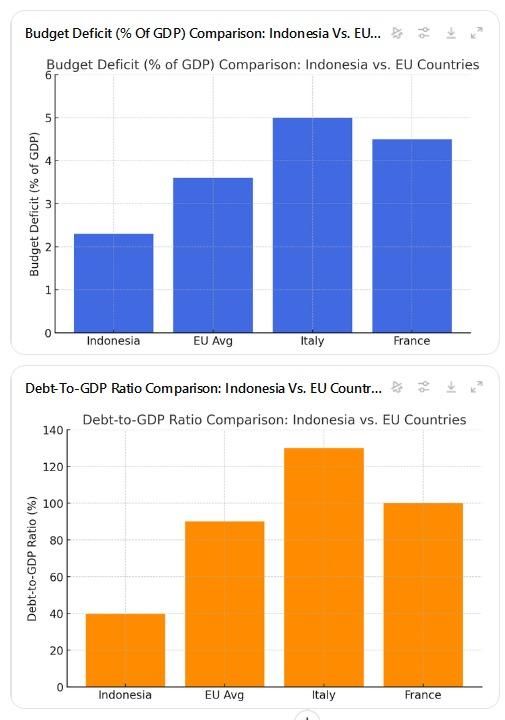

While increasing the debt-to-GDP ratio and budget deficit may raise concerns, it's important to note that many developed economies, particularly in Europe, operate with much higher deficits. In 2023, the average budget deficit among EU countries was approximately 3.6% of GDP, with some nations like Italy and France running deficits of 4.5-5%. By comparison, Indonesia's current deficit of around 2.3% is conservative. The proposed increase to 5% would still place Indonesia well within the range of many developed economies, especially when paired with infrastructure investments and social spending (Table 1).

{kind=link}

{kind=link}

Moreover, the plan to increase Indonesia's debt-to-GDP ratio to 50% remains well within the legal limit of 60%, established under Indonesia's fiscal law. This provides ample room for responsible borrowing, provided the funds are used for growth-enhancing projects. Many countries, including those in the EU, have debt-to-GDP ratios exceeding 90-100%, further illustrating that Indonesia's planned increase remains sustainable if paired with strong growth and prudent fiscal management (Table 2).

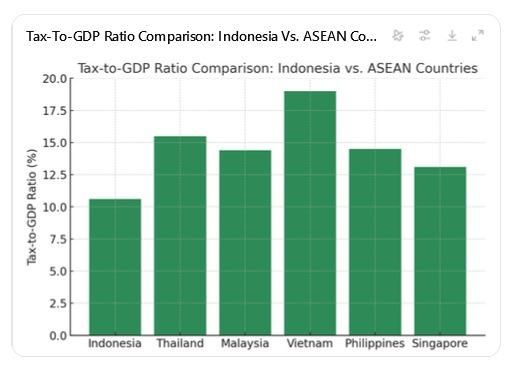

In addition, Indonesia's tax-to-GDP ratio of 10.6% is significantly below the ASEAN average of around 15%. Countries like Thailand and Malaysia have tax-to-GDP ratios of 14-16%, while Vietnam stands at about 19% (Table 3). Raising Indonesia's ratio to 16% would align it more closely with regional peers and help fund critical infrastructure and social services.

These plans build on the solid foundation laid by prior economic reforms, which have kept Indonesia's fiscal situation on solid footing. However, in considering three potential scenarios-gradual increase, rapid increase, and shock increase-it becomes clear that each carries different risks and rewards for Indonesia's economy, inflation, currency value, and credit rating.

Scenario 1: The Gradual Approach

In this scenario, the debt-to-GDP ratio would increase by 2-3% annually, reaching 48-49% within five years, accompanied by a gradual rise in the budget deficit and tax-to-GDP ratio. The slow pace allows the government to spread borrowing over time, reducing the risk of a sudden surge in debt servicing costs.

Real GDP growth of 3.5-4% per year, with nominal GDP growth of 7-9%, is needed to keep the debt manageable. Continued investment in infrastructure would boost productivity and support long-term economic growth.

However, risks remain. A modest increase in debt will likely push bond yields slightly higher, potentially reaching 7-8%, and inflation could rise to 6-7%. The rupiah, currently trading at 15,300 IDR/USD, may depreciate by 3-4%, reaching 15,750-16,000 IDR/USD. This would lead to a minor increase in import costs but keep currency stability intact.

A 1-notch downgrade remains a possibility if growth falters or global conditions deteriorate, but the overall fiscal outlook would remain stable under this scenario.

Scenario 2: The Rapid Increase

In this scenario, Indonesia's debt-to-GDP ratio would rise by 3-4% annually, reaching 50% within 2-3 years. The budget deficit would climb quickly to 5%, while the tax-to-GDP ratio would increase within 4-5 years. This faster pace offers more immediate fiscal resources but raises concerns about debt sustainability.

To avoid a credit downgrade, Indonesia would need nominal GDP growth of 9-10%, with real GDP growth of 4-5%. Anything less could lead to a dangerous cycle of rising debt and interest payments. Inflation could hit 7-8%, eroding consumer purchasing power, and bond yields would likely rise to 7-8%, further straining the budget.

The rupiah would face greater pressure, depreciating by 5-7%, bringing the exchange rate to 16,000-16,400 IDR/USD. A 7% depreciation would add 1,070 IDR per USD, increasing import costs and inflationary risks. The risk of a 1-notch downgrade is high if real growth does not exceed 4%, making borrowing more expensive and raising doubts about long-term fiscal sustainability.

Scenario 3: The Shock Increase

In this aggressive scenario, Indonesia's debt-to-GDP ratio would surge by 5% or more per year, reaching 50-53% within just 1-2 years. The budget deficit would hit 5% immediately, and the tax-to-GDP ratio would need to rise sharply over the next 3-4 years. This approach would provide immediate resources - about USD100B per year - but at a significant cost.

To avoid a 1-2 notch downgrade, Indonesia would need nominal GDP growth of 10-12%, with real growth of 6-7%-a challenging target given current global conditions. Bond yields could spike to 8-9%, making debt servicing far more expensive and leaving less room for social programs and infrastructure spending.

Inflation could soar to 8-10%, and the rupiah would be under severe pressure, potentially depreciating by 7-10%, pushing the exchange rate to 16,400-16,800 IDR/USD. A 10% depreciation would add 1,530 IDR per USD, raising import costs and further worsening inflation. Such a sharp drop in the rupiah's value would increase the burden of foreign-denominated debt, straining government finances and potentially triggering capital outflows.

Balancing the Risks and Rewards

Each of these scenarios presents different risks and rewards. A gradual approach offers stability, minimizing the risk of credit downgrades, currency depreciation, and inflation. A rapid or shock increase could lead to faster short-term growth but risks inflation spikes, significant currency depreciation, and downgrades.

President Prabowo's administration must strike a balance between aggressive fiscal expansion and prudent fiscal management. His ambitious goals can be achieved without destabilizing the economy, but careful management of debt, the deficit, and revenue streams is essential.

Ultimately, Indonesia's future success will depend on its ability to foster sustained economic growth, boost productivity, and control inflation. Only by achieving these goals can Prabowo ensure his expansionary policies lead to long-term prosperity.

Eduardo Araral, Associate Professor PhD (Public Policy) Indiana University-Bloomington

(ncm/ega)